In December 2022, the European Central Bank (ECB) released its Eurosystem Staff Macroeconomic Projections for the Euro Area. With well-documented economic influences already leading to a sharp slowdown in real GDP growth in the third quarter of 2022, the main forecast was: The expectation of a short-lived and shallow recession in the euro area at the turn of the year. We take a look in detail at the ECB’s latest forecasting on inflation.

- The current situation

- The latest inflation forecasts from the European Central Bank

- How do the EU predictions compare with other institutions

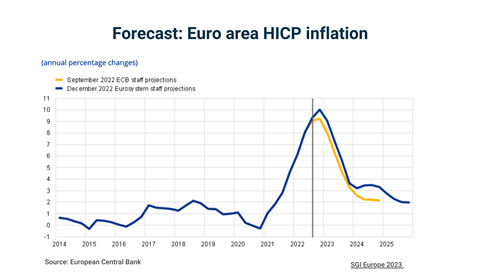

The key message: Inflation is expected to fall steadily in 2023, to 6.3%, and to 3.6% in the last quarter of 2023

Overview

- consumer and business confidence remain subdued

- real disposable incomes are still being eroded

- soaring cost pressures are curtailing production, especially in energy-intensive industries

However, these negative economic repercussions are expected to be partially mitigated by fiscal policy measures.

In the medium term, the Eurosystem report* makes the following predictions:

- energy markets are expected to rebalance

- uncertainty will decline

- real incomes will improve

- foreign demand is expected to strengthen

- supply chain bottlenecks are expected to resolve

As a result, economic growth is expected to rebound, despite less favorable financing conditions.

Focusing on Inflation

Focusing on headline inflation (i.e., the change in the value of goods in a consumer’s basket) and the harmonized index of consumer prices (HCIP) to measure consumer price inflation across all countries in the EU, the latest report forecasts:

- The short-term outlook for inflation remains surrounded by high uncertainty

- HICP inflation is expected to stay extremely elevated in the short term (revised up from the September 2022 projections)

- Inflation is expected to fall steadily in 2023, to 6.3%, and to 3.6% in the last quarter of 2023

- Inflation is expected to decline to an average of 3.4% in 2024

- Inflation is expected to decline to an average of 2.3% in 2025

Factors driving the persistence include: Indirect effects from high energy prices; the past sharp depreciation of the euro (despite the recent slight appreciation); and robust labor markets and inflation compensation effects on wages (which, although expected to grow, will in real terms, remain below the levels seen before the war in Ukraine).

Good news for manufacturers: Energy inflation will fall sharply in the course of 2023. And for retailers, this will contribute significantly to the decline in the headline inflation rate. However, energy inflation will remain an important factor in headline inflation being significantly above the ECB’s inflation target in 2024.

How do the Eurosystem predictions compare with other institutions

Of comparisons forecasts from other international organizations and private sector institutions, the report states: “These forecasts are not directly comparable with one another or with the Eurosystem staff macroeconomic projections.”

However, they add that the December 2022 Eurosystem staff projections are “at the upper end or above other forecasts for both GDP growth and inflation over the entire horizon, and the projections for growth are slightly above the range of other forecasts for 2022 … For 2023 and 2025 they are within the range, while for 2024 the Eurosystem staff projections are the highest. As regards inflation, the Eurosystem staff projections are within the range of other forecasts for 2022 and 2023 and at the upper end or above the range for 2024 and 2025.”

* Eurosystem is the central banking system of the EU, comprising the European Central Bank and the national central banks of EU member states whose currency is the Euro. You can read the full report here.