An earnings beat couldn’t contain the damage: Nike’s Q3 figures confirmed that tariff-driven margin pressure and a deepening China retreat are structural, not cyclical — and investors responded by pushing the stock to its lowest point since 2014.

Nike’s fiscal third-quarter results, released on March 31, 2026, delivered exactly the kind of split verdict that unsettles markets: numbers that technically beat expectations, paired with forward guidance that made the beat look beside the point. In the five trading days since, the stock has shed more than 15 percent of its value, falling to levels not seen since 2014.

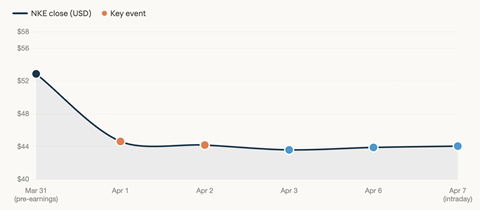

The story is most clearly told through the share price trajectory:

The numbers behind the selloff

For the quarter ended Feb. 28, 2026, Nike reported revenue of $11.28 billion (€10.37 billion at current indicative rates), flat year on year on a reported basis and down 3 percent in currency-neutral terms. Net income fell 35 percent to $520 million.

Attention centered on margin. Gross margin came in at 40.2 percent, down 130 basis points from a year earlier. Chief Financial Officer Matt Friend said tariffs in North America accounted for a 300-basis-point drag within that decline, as the company absorbs the impact of a 10 percent global baseline tariff introduced after a Supreme Court ruling in February overturned the prior emergency-powers framework. Operating cash flow fell 68 percent to $579 million, reflecting, among other items, a $230 million severance charge tied to restructuring across supply chain, technology and Converse operations.

Guidance was where the floor gave way

In another market, the earnings beat might have been enough to steady the shares. This time, it was the outlook that drove the reaction. Nike told investors to expect fourth-quarter fiscal 2026 revenue to fall 2 to 4 percent, against consensus expectations for 1.9 percent growth.

Management also signaled a sharper pullback in Greater China, guiding to an approximately 20 percent decline for the quarter as it reduces sell-in and continues marketplace “cleanup.” For calendar 2026, Nike is guiding to a low-single-digit revenue decline, with North America growth insufficient to offset the contraction in China.

On the earnings call, CFO Matt Friend said margin improvement is unlikely before the second quarter of fiscal 2027, and only if tariff mitigation efforts such as supply chain diversification and selective price increases gain traction. Another risk sits outside the current outlook: Section 301 investigations underway into Vietnam, Bangladesh, Cambodia, and India, which could widen tariff exposure further.

A stock at levels not seen since 2014

On April 1, the first full trading session following the release, Nike’s stock fell more than 15 percent, the sharpest single-day decline since 2024, closing at approximately $44.63. By April 2, further price-target cuts from sell-side analysts pushed the close to $44.19, with an intraday low of $43.17 — its lowest point in 12 years.

The 52-week high stands at $80.17, meaning the stock has lost nearly half its value over 12 months.

At the time of writing on April 7, shares were trading around $44, within the day’s range of $43.56 to $44.38. Goldman Sachs reduced its price target earlier today, citing what it described as limited near-term valuation support. The consensus analyst picture is not uniformly bearish: according to Reuters, 25 analysts covering Nike carried an average buy rating with a 12-month target of $75.25, implying substantial upside from current levels — and the company holds $8.1 billion in cash with 24 consecutive years of dividend increases.

What Nike’s selloff signals for the sector

Nike’s tariff-driven margin squeeze is also a proxy for the pressure building across the athleticwear industry. Rival brands have issued similar warnings: Under Armour has projected an additional $100 million in tariff-related costs in fiscal 2026, while Lululemon Athletica has forecast a $380 million hit for the year. Adidas has also flagged the impact of higher duties on sourcing-heavy categories.

The vulnerability is structural. More than 90 percent of footwear and apparel for the biggest global brands is made in Vietnam, Indonesia, Cambodia and China — countries now facing some of the steepest duty rates. Companies continue to talk up diversification, but shifting production to India, Latin America or North Africa is a multi-year project, not a single-season fix.

Taken together, Nike’s Q3 read-through suggests the tariff shock is less a short-term headwind than a reset to the industry’s margin baseline, with recovery likely to play out over fiscal years rather than quarters.