L.E.K. Consulting’s fifth annual Brand Heat Index tracks upward momentum across 650 brands — and the 2026 data points to a structural shift: premium challengers are closing on legacy leaders faster than at any point in the index’s history, with generational segmentation now the critical variable.

A new annual survey of around 6,000 US consumers finds competition at the top of key sporting goods categories at its most intense in five years, with premium challengers narrowing the heat-score gap on established leaders and Gen Z driving faster brand churn than any previous cohort. The data has direct implications for brand, buying and ranging decisions in the sporting goods market globally.

Published March 3, 2026, L.E.K. Consulting’s fifth annual Brand Heat Index surveyed approximately 6,000 US consumers aged 14 to 55 who had purchased footwear, apparel or accessories within the previous 12 months. Around 650 brands were scored on a standardized 0–100 index measuring upward popularity trajectory – not size – across athletic, casual, outdoor and dress categories in footwear and apparel, plus bags & luggage and outdoor equipment & sporting goods (the latter two appearing in the index for the first time this year).

The headline finding: competition at the top has intensified significantly.

In 2026, seven out of 16 tested apparel and footwear categories saw their top three brands fall within 10 heat-score points of each other – up from just four such categories in 2025. Across all categories that matter to the sporting goods industry, the same pattern recurs: premium technical challengers are closing rapidly on legacy leaders, social media is reshuffling brand relevance at generational speed, and the brands best positioned for sustained growth are those operating with clear consumer segmentation rather than broad mass appeal.

“The brands rising fastest and cutting through the noise are those speaking directly to core sets of consumers rather than trying to be everything to everyone,” said Laura Brookhiser, L.E.K. Managing Director and lead author of the report.

“But success here isn’t just a marketing challenge – it’s about how brands configure their entire business, from product development to pricing, all to reinforce differentiation and resonance with their target consumer.”

To extract what matters most for the sporting goods industry, SGI Europe has filtered the data by relevant categories. Here are the highlights – the full 27-page report is available to download here.

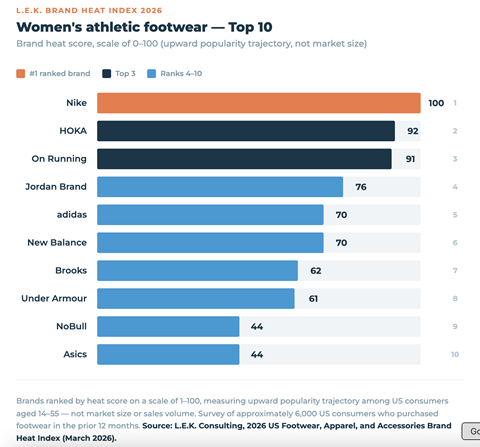

Athletic footwear: Nike holds, but the margin is narrowing

Nike retains the top position in both women’s and men’s athletic footwear, but the lead is far less comfortable than it once was. In women’s, HOKA and On Running sit within nine points of Nike’s 100-point index score, forming a tightly clustered trio at the top. Among Gen Z women, Nike and On Running are tied for first; among Gen X women, HOKA has displaced Nike as the top brand.

The broader structural shift in athletic footwear belongs to running-heritage brands. New Balance and Brooks have registered meaningful heat-score gains across age groups.

Asics enters the women’s top 10 this year, propelled by notably strong performance among Gen Z – a cohort that L.E.K. identifies as more open to performance brands with technical credibility and social media presence than to heritage lifestyle labels.

On the men’s side, Nike, Jordan Brand and adidas continue to hold the top three positions overall, but HOKA, New Balance and On Running are steadily closing the gap. Notably, HOKA has become the second-ranked brand among Gen X men. The most significant directional loser: Under Armour, which has dropped from fourth to seventh place overall in men’s athletic footwear as performance running brands absorb share of attention.

The strategic implication is clear. The athletic footwear category is no longer a two-brand race. Any brand or retailer building assortments around Nike and adidas alone is missing the consumer momentum that is aggregating around running specialists. Premium positioning, technical credibility and generational relevance – particularly with Gen Z and Gen X – are the differentiating variables.

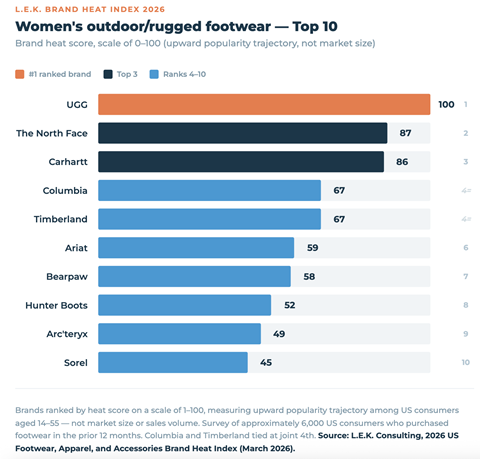

Outdoor footwear: Arc’teryx and Salomon make their move

In outdoor and rugged footwear, established workwear and heritage brands continue to anchor the category, but the most notable development is the upward trajectory of premium technical labels.

Arc’teryx and Salomon are the index’s top gainers in men’s outdoor footwear this year. Arc’teryx rises to fourth overall in men’s outdoor – and to the same position among Millennials and Gen X – while Salomon claims sixth overall with particular strength among Millennials. Both represent a premium technical positioning that is gaining traction with consumers who are no longer satisfied with mainstream outdoor labels for their off-trail or mountain activities.

The men’s category overall is led by Carhartt, which has surpassed Timberland to take the top position (except among Gen Z, where Timberland still leads). Columbia holds firm in third. On the downside, CAT Footwear drops out of the top 10 overall and UGG slides to tenth in men’s outdoor – a signal that its crossover into this segment may be softening.

Women’s outdoor footwear tells a different story. UGG remains No. 1 overall, and the top of the women’s list skews toward winter lifestyle brands. The North Face holds second overall but its scores are softening. Carhartt shows increased strength, particularly with Gen Z and Gen X women where it achieves the top position. Merrell, by contrast, has dropped out of the overall women’s top 10, though it persists on Millennial and Gen X lists – a sign of generational audience maturation rather than outright decline.

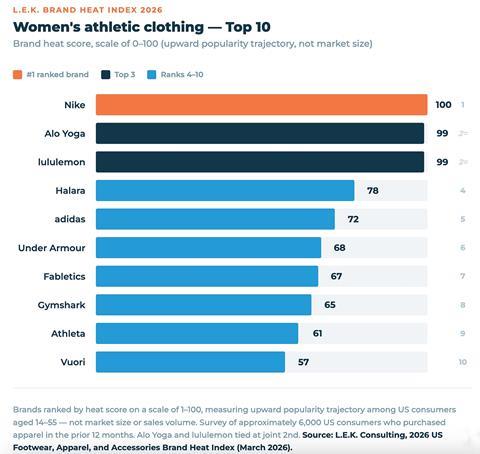

Athletic clothing: Alo Yoga rewrites the challenger playbook

Nike retains the No. 1 position in both women’s and men’s athletic clothing overall, but the gap with second place is the thinnest the index has recorded. Among women, Alo Yoga and lululemon both score 99 against Nike’s 100 in the overall index. Among Gen Z women specifically, lululemon and Alo Yoga jointly take the top spot, with Nike slipping to third.

The performance of Alo Yoga is arguably the defining brand story of the 2026 index. Alo Yoga’s rise has not been confined to women. It has translated female momentum into men’s market share, entering the overall men’s top 10 and landing as the No. 2 brand for Gen Z men. Chris Randall, L.E.K. Managing Director and co-author, described this as an inversion of the traditional gender extension model:

“We’ve seen an interesting shift happening with Gen Z men, where the traditional playbook of launching male-first and extending to women is being flipped. Female-focused brands, like Alo Yoga, are successfully scaling by winning with younger male consumers who are more open to brands that weren’t originally designed for them.”

TikTok-driven brands are making their presence felt across the category. Halara, which achieved viral visibility through the platform, debuts in the women’s index at fourth overall and shows consistent heat across generations. This is the clearest evidence in the report that social media reach is now a structural brand-building asset, not just a marketing channel. Among Gen Z particularly, L.E.K. identifies a strong social presence as a core driver of heat scores across multiple categories.

Among men, the legacy trio of Nike, adidas and Under Armour holds the top three positions, but Gymshark and Vuori are gaining ground. The counterpoint: brands that were riding momentum in 2025 but have not maintained it include Girlfriend Collective and Champion, both of which fall out of the women’s top 10 entirely.

Outdoor clothing: luxury outerwear breaks into the mainstream top 10

The North Face holds the top position in outdoor clothing for both women and men and across all generational cohorts – the only brand in the index to do so consistently. But the strategic story in outdoor apparel in 2026 is the sustained rise of luxury outerwear.

Moncler enters the men’s overall top 10 at second place, driven by a first-place finish among Gen Z men. On the women’s side, four luxury and premium outerwear brands – Moncler, Mackage, Canada Goose and Moose Knuckles – all make the overall top 10.

This is a category-wide shift toward what the report describes as the “hourglass economy”: outside of casual categories where accessible pricing and fast fashion dominate, premium brands are giving consumers a reason to trade up and the heat data reflects that willingness.

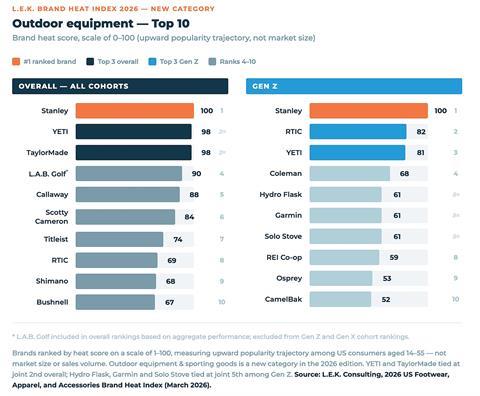

Outdoor equipment: Stanley and YETI lead a generationally divided category

Making its debut in the Brand Heat Index in 2026, the outdoor equipment & sporting goods category is the most generationally fragmented in the entire index. Across all cohorts combined, Stanley ranks first overall and YETI second — but beneath that headline, the data reveals three almost entirely distinct brand universes depending on the age of the consumer. What “outdoor” means, and which brands carry authority within it, shifts dramatically from one generation to the next.

For Gen Z, outdoor identity is expressed through lifestyle accessories and brand association as much as through activity-specific performance gear. Stanley leads among this cohort, with YETI, Hydro Flask and Coleman also featuring prominently — brands that signal an accessible, social-media-native relationship with the outdoors rather than a commitment to any particular sport or discipline. Garmin is the notable exception, making the Gen Z top 10 on the strength of GPS wearables for fitness tracking — a reminder that performance technology with a strong visual identity can cut through even in a lifestyle-dominated cohort.

Among Millennials, the category profile shifts decisively toward sport-specific performance equipment. YETI tops the Millennial list, but the brands around it reflect a far more activity-oriented consumer: golf, snow sports and cycling brands all feature prominently.

What the data means: a brief strategic read

The clearest message across all five categories is directional: the gap between legacy leaders and premium challengers is narrowing, and it is narrowing fastest among younger consumers. Heat scores measure trajectory, not size — and the trajectory of brands like On Running, HOKA, Arc’teryx and Alo Yoga is consistently upward, while several established names show signs of generational erosion that aggregate scores can mask.

The second consistent pattern is the role of social media — particularly TikTok — as a structural brand-building channel, not just a marketing add-on. Brands that broke into top 10 positions primarily through platform-driven awareness, rather than traditional sponsorship or retail presence, are a feature of almost every category in this edition.

For a full breakdown by category, generation and gender — including men’s rankings — the complete report is available directly from L.E.K. Consulting here: L.E.K. Consulting 2026 US Footwear, Apparel, and Accessories Brand Heat Index.

Factfile

The 2026 Brand Heat Index is the fifth annual edition of L.E.K. Consulting’s US consumer survey, published March 3, 2026. It is based on responses from approximately 6,000 US consumers aged 14 to 55 who had purchased footwear, apparel, bags & luggage or outdoor equipment & sporting goods for themselves in the prior 12 months. Around 650 brands were evaluated across athletic, casual, outdoor/rugged and dress categories in both footwear and apparel, with bags & luggage and outdoor equipment & sporting goods appearing as standalone categories for the first time in this edition. Each brand receives a standardized score of 0 to 100 reflecting upward popularity trajectory relative to other brands in its category – not market size or sales volume. Results are segmented by gender and by generational cohort: Gen Z, Millennial and Gen X.