In Q1, ended March 31, the company reported 4.1 percent operating income growth to $46.5 million.

Columbia Sportswear CEO Tim Boyle tells analysts that the group does not know “what the consumer is going to be doing in the back half of the year” and has no idea what its final product costs for fall 2025 and spring 2026 will be at this point, as the brand withdraws its FY25 outlook. In early February, the group estimated annual sales growth of 1 to 3 percent, which included single-digit sales increases in both EMEA and the US.

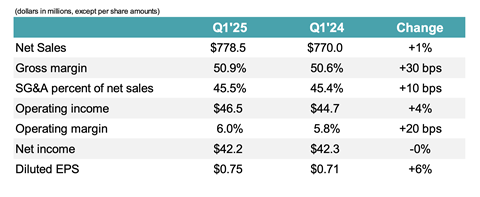

In Q1, ended March 31, the company reported 4.1 percent operating income growth to $46.5 million from a 1.1 percent net sales gain to $778.5 million. Year-over-year net income was flat at $42.2 million, and gross margin increased by 30 basis points to 50.9 percent.

With plans to introduce a new global marketing platform in August that “will be the Columbia brand character and voice for years to come,” Columbia estimates that the 10 percent universal tariff and the higher tariffs for China implemented by the US would add $40 to $45 million to the cost of sales for the fall season. The company does not expect to offset these higher costs this year. Instead, its mitigation strategy will evolve in response to trade policy changes. Given the current global climate, the company anticipates the US market will be challenging in H2 and that retailers will be cautious when placing orders.

Turning to markets outside the US, Columbia said it was not possible “to predict the extent to which US tariff actions will impact international economic growth and consumer demand” for its products.

Wholesale revenues increased by 4 percent on a constant-currency basis to $400 million in Q1, driven by higher spring ’25 orders, and reported DTC sales were flat at $378 million. Apparel/Accessories/Equipment sales increased by 2 percent to $629 million; Footwear sales slipped by 1 percent to $149 million.

By brand on a reported basis, Columbia sales rose 3 percent to $683 million, with all markets growing except for Canada. Sorel sales dipped 8 percent to $42 million; prAna revenues fell by 10 percent to $28 million; and Mountain Hardwear sales slipped by 14 percent to $25 million.

Regionally, Q1 revenues increased in EMEA and LAAP, but fell in both the US and Canada. EMEA sales were up 7 percent, as direct net sales rose by a high-single digit, with growth in all channels led by DTC stores. The EMEA distributor business was down slightly despite strong spring orders due to a timing shift.