A new Deloitte report maps the trajectory of a $3 billion market. SGI Europe translates the numbers into strategic intelligence for brands, retailers, and licensing executives.

The headline figure from Deloitte’ s latest analysis of women’s elite sports is striking: global revenues are forecast to reach at least $3.04 billion (approximately €2.8 billion) in 2026 – a 25 percent increase on the $2.4 billion generated in 2025, and a 340 percent rise from the $692 million recorded in 2022. More than the numbers, the structural shifts beneath them matter, and so do the demands they place on an industry that supplies the kit, equipment and merchandise behind it.

| Revenue source | 2022 | 2026 (projected) | Change 2022–2026 |

|---|---|---|---|

| Matchday | 11% ($76M) | 30% ($912M) | +1,100% |

| Broadcast | 25% ($173M) | 25% ($760M) | +339% |

| Commercial | 64% ($443M) | 45% ($1,368M) | +209% |

| Total | US$692M | US$3.04B | +340% |

Sponsorship is the growth engine – and non-endemic brands are accelerating

Commercial revenue – comprising sponsorship, partnerships and merchandising – is now the single largest revenue category in women’s elite sports, projected at 45 percent of total revenues in 2026, or approximately $1.37 billion (€1.26 billion). That category grew in absolute terms by more than $250 million in a single year, according to Deloitte’s analysis.

What is changing is who is showing up as a sponsor. Fashion, beauty, and technology companies are entering at scale alongside traditional sports partners. In December 2025, the Women’s Tennis Association (WTA) announced Mercedes-Benz as its Premier and Exclusive Automobile Partner, with the car manufacturer reportedly committing $50 million per year for up to a decade. That deal is structurally illustrative: one of the world’s most established automotive brands chose women’s tennis over a range of alternatives. For sporting goods companies, the competitive landscape for sponsorship in women’s sports is expanding beyond their traditional peer group, and first-mover advantage is eroding quickly.

One data point from the broader report stands out: across US college sports between 2022 and 2024, women’s sports revenue grew 4.5 times faster than men’s, driven by brand demand and increased visibility. That trajectory is not limited to North America.

| Soccer | Basketball | Other | Total | |

|---|---|---|---|---|

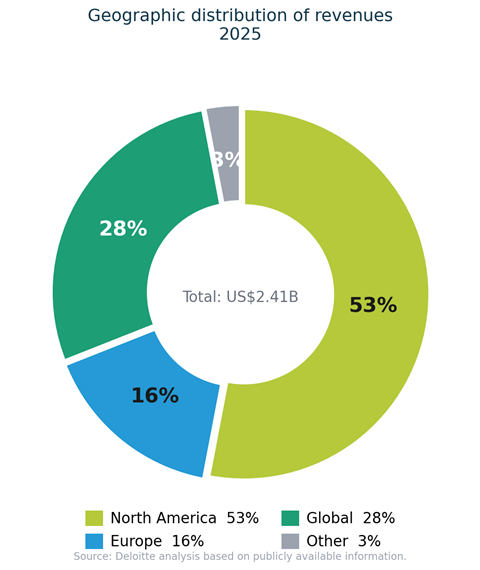

| 2025 | 37% ($892M) | 32% ($771M) | 31% ($747M) | US$2.41B |

| 2026 (projected) | 35% ($1,064M) | 35% ($1,064M) | 30% ($912M) | US$3.04B |

| Change | +19% | +38% | +22% | +26% |

League independence rewrites the commercial contract

Some of the report’s most consequential findings are structural. Women’s leagues are separating from national governing bodies at an accelerating pace. England’s WSL Football (Women’s Super League) is in its second year as an independent entity overseeing the top two tiers of English women’s football; Germany’s Frauen Bundesliga is reportedly completing a comparable spin-out from the German Football Association (DFB), with league clubs holding a 50 percent stake in the new venture.

Independence matters commercially because autonomous leagues hold their own commercial rights – including kit supply agreements, licensed merchandise programs and brand partnerships. An independent WSL or Frauen Bundesliga is a potential partner on its own terms, not a subordinate division of a men’s structure with different commercial priorities.

At club level, the pattern is reinforced by investment. Tech entrepreneur Alexis Ohanian’s minority stake in Chelsea FC Women – following a structural separation that valued the women’s team at a reported £200 million (approximately €234 million) – and a minority investment in Aston Villa Women by Marc Zahr, co-president of Blue Owl Capital Inc., demonstrate that standalone valuations are attracting sophisticated capital. As those valuations rise and structural clarity improves, kit and merchandise deals will be priced accordingly.

Football and basketball together are expected to account for 70 percent of all women’s sports revenues in 2026 – 35 percent each.

Soccer’s projected growth, Deloitte notes, will be driven by leagues becoming independent and by club governance restructuring that positions women’s teams alongside, rather than beneath, their men’s counterparts.

Facility investment is locking in long-term equipment demand

The Deloitte report identifies infrastructure spend as a primary valuation driver – and it carries direct implications for product and equipment demand. At least five WNBA (Women’s National Basketball Association) organizations have announced new training facilities, including a reported $150 million commitment for the Los Angeles Sparks, described as the largest single-team infrastructure investment in the history of women’s sports. In the UK, London City Lionesses – part of Michele Kang’s Kynisca multi-club ownership group – have announced a performance campus designed specifically around the physiological requirements of female athletes.

Dedicated facilities translate into equipment procurement cycles, product testing partnerships, and supply relationships of a duration and scale that casual kit deals do not. The message in the infrastructure data is that women’s sports organizations are building to last – and they will need products built to match.

The WNBA’s recently signed $2.2 billion, 11-year media rights deal – the largest in women’s sports history – reinforces the same message. Broadcast commitments on that scale lock in commercial ecosystems for many seasons.

The consumer is ready; and the product ecosystem?

The Deloitte report profiles the women’s sports fan base as younger, more digitally native and more family-oriented than traditional sports audiences. Critically for the sporting goods sector, women fans show high purchasing intent: they are typically the lead household spenders. The problem is supply. Suitable, desirable merchandise options remain scarce across most women’s sports properties.

That gap is a market waiting to be claimed. The Style of Our Own pop-up in London during summer 2025 – which brought together more than 20 community-centric women’s sports brands – demonstrated that a community-focused retail model can generate genuine commercial energy independent of established retail infrastructure.

The consumer is ready; the product ecosystem has not caught up.

The geographic breakdown raises the stakes for European industry players. North America accounts for 54 percent of total women’s sports revenues in 2026 ($1.64 billion; approximately €1.51 billion). Europe, at 14 percent ($434 million; approximately €400 million), is the most consequential near-term expansion zone for sporting goods brands based in Germany, France, Switzerland and the UK. The WSL’s planned growth from 12 to 14 teams for the 2026/27 season and the Frauen Bundesliga’s structural transition are inflection points with direct commercial consequences for European suppliers.

What this means for the sporting goods industry

For established brands: Deloitte’s central structural finding – that women’s sports is forging a distinct identity rather than replicating a smaller version of the men’s game – should reconfigure how brands approach product development, licensing and sponsorship activation.

Sponsorships and marketing in women’s sports, the report argues, must not simply follow the men’s template; they must speak to an engaged audience with divergent preferences. Brands that transpose men’s commercial models without adaptation will underperform against those that build women’s-specific commercial architectures from the ground up.

For challengers and new entrants: The licensing white space identified in the report – particularly in merchandise – is the most immediate opportunity. Community-retail formats, direct partnerships with newly independent leagues, and early-stage investment in athlete NIL (Name, Image, and Likeness rights) and endorsement agreements are the levers most likely to generate durable returns as the market matures.

The report notes that the fan base for women’s sports often brings in new-to-sport consumers rather than cannibalizing existing audiences – this is an additive market, not a zero-sum competition.

Timing and opportunities: Jennifer Haskel, Knowledge & Insights Lead at Deloitte’s Sports Business Group, offers the calibration that executives should hold in mind:

“However, it is important to recognise that it is still early days. Building a sustainable cultural and economic identity requires strategic investment, patience, and innovation. The industry’s enduring success will be built on diligently collecting data, analysing its impact, and making corrections driven by these learnings.”

Deloitte’s 2026 report Game Changers: Unlocking the Potential of Women’s Sports (April 2026) examines the fast-growing women’s elite sports economy, sizing revenues across matchday, broadcast and commercial streams. The full report can be downloaded here.