The retail and investment group is driving forward its corporate restructuring with further acquisitions and international expansion. At the same time, margins and retail profit are improving – yet the British company is deliberately refraining from providing a forecast for FY27.

Frasers is moving at pace: Takeover bids for Hugo Boss and Accent Group, international expansion, and prompting the group to withhold FY27 guidance – the retail and investment group has its hands full right now. At the same time, the company is also grappling with weak consumer sentiment and high inventory levels in the market. Operationally, however, there is momentum: margins and retail profit have risen significantly – another sign that the Elevation Strategy is taking hold.

“The Elevation Strategy is going from strength to strength.” CEO Michael Murray

Positive feedback from brand partners and customers confirms that the group is on the right track. With Flannels, international sports operations, a growing real estate portfolio, Frasers Plus, and strategic investments, the group has significantly restructured its business in recent years: The owner of the Sports Direct retail chain has long since evolved into a broadly diversified retail group.

Group revenue on track

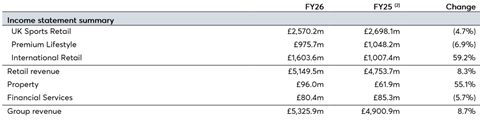

The results for FY26 underscore this trend: Revenue rose by 8.7 percent to £5.33 billion (€6.23bn). Retail profit rose by 22.1 percent to £912.5 million (€1.07bn), while the retail gross margin improved by 150 basis points to 47.1 percent.

A minor setback, however, came from the largest business division of all: In the UK Sports segment, revenue fell by 4.7 percent to £2.57 billion (€3.01bn). However, this trend does not reflect Sports Direct’s business alone. The segment also includes the UK online sports business, Everlast Gyms, Studio Retail, and other sports and wholesale activities. The company attributes the decline in revenue primarily to the planned closure of Game UK standalone stores and Studio Retail. At the same time, the segment’s gross margin improved by 290 basis points to 51.1 percent, and trading profit rose by 17.6 percent to £559.4 million (€654m). This exemplifies the goal of the Elevation Strategy: lower revenue in lower-margin areas, but significantly higher profitability.

Premium: lower revenue, higher margin

The Premium Lifestyle segment, which includes Flannels, Frasers, House of Fraser, Cruise, Jack Wills, Van Mildert, Gieves & Hawkes, and Sofa.com, generated revenue of £975.7 million (€1.14bn). Revenue declined by 6.9 percent, while the gross margin increased significantly thanks to a stronger product mix and a recovery at Flannels.

Expansion pays off

International growth engine: This division grew by 59.2 percent to £1.60 billion (€1.88bn) thanks to the acquisitions of XXL and Holdsport. This now accounts for 30 percent of revenue, up from just over 20 percent in the previous year. The Property and Financial Services segments also contributed an additional £96.0 million (€112m) and £80.4 million (€94m), respectively, to consolidated revenue.

Frasers Plus: The new growth driver

“We remain focused on the growth opportunities being created across the Group,” Murray emphasizes. These include a stronger product and brand mix at Sports Direct, international expansion, the positive performance at Flannels, the growing real estate portfolio, and Frasers Plus. The number of active customers in the company’s in-house credit and loyalty program rose from 0.6 million to 1.1 million during the fiscal year.

A rapid shopping spree

While the core business is making good progress, Frasers is simultaneously pushing ahead with its restructuring at a rapid pace. During the fiscal year, the Group acquired the South African sports retailer Holdsport and the Nordic retailer XXL, invested in the U.S. luxury multi-brand retailer The Webster, and expanded its real estate portfolio with additional shopping centers and outlet locations.

No forecast, clear direction

Despite all the progress, the CEO remains cautious. The company continues to feel “the impact of tough trading conditions, subdued consumer confidence, and industry-wide excess inventory levels,” which had already become apparent in the second half of the year and extended into the start of FY27.

After the balance sheet date, however, Frasers stepped up its efforts once again and launched takeover bids for Hugo Boss and the Australian sports retailer Accent Group. The outcome is currently uncertain. Furthermore, the group sold Sports Direct Malaysia to its long-standing partner Map Active. It also acquired Hervis’s Romanian and Hungarian retail operations. In light of these transactions, management is currently deliberately refraining from providing a forecast for FY27. Anyone expecting the company to shift into a lower gear will be disappointed. Frasers is sticking to its expansion course and accelerating its restructuring with further acquisitions, equity investments, and real estate investments – despite a market environment that Murray himself describes as challenging.

This expansion strategy is made possible, among other things, by an operating cash flow of £946.4 million (€1.11bn) and a credit facility expanded to £3.3 billion (€3.86 billion). Net debt did rise to £1.17 billion (€1.37bn). The strategy is thus clearly defined: Frasers does not intend to sit out the current market weakness, but rather to use it to further expand its position as an international retail and investment group.