The week ending June 15 – NBA Finals, World Cup group stage – was the largest in Kalshi’s history. Total trading volume reached $8.99 billion, of which 86.9 percent was sports. That single week exceeded all of Kalshi’s 2023 volume combined. How did a federally regulated exchange for binary event contracts become, in effect, the largest sports-betting operation in the United States? Not by accident.

For its first four years Kalshi traded exclusively in politics, economics and other non-sports categories. Sports appeared on the platform for the first time in December 2024, and it was a quiet debut. The real activation came in February 2025, with the Super Bowl. Sports claimed 39 percent of that week’s $68 million in total volume. March Madness, the NCAA’s college-basketball tournament, pushed the share past 90 percent. And the next NFL season, begun in September 2025, set it above 87 percent, where it stayed.

Exotics?

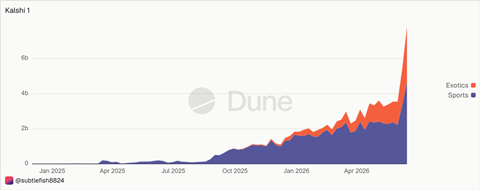

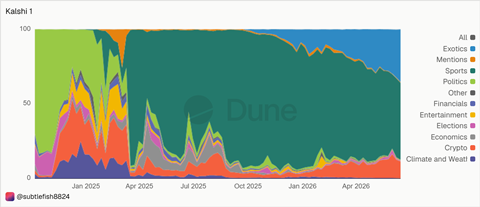

Dune data – drawn from Kalshi’s public API, aggregated by Dune Analytics, queried by SGI Europe – puts sports’ lifetime share of volume through June 15 at roughly 85 percent of an approximately $112 billion total. That figure combines two Kalshi categories: Sports ($73.9 billion, in 1,949 markets) and Exotics ($20.9 billion, in ten markets). The second category is the more instructive .

Exotics looks, at first glance, like diversification. It is not. An examination of all 100 available rows of Exotics data by contract type shows three ticker types throughout: multi-game extended sports parlays, cross-category sports combiners and college-basketball championship markets. Every contract in the category derives from sport. Exotics is a product, a range of more complex sports instruments, not a miscellaneous bin. It emerged in mid-September 2025, coinciding with the NFL season opener, and – rather than displace single-game contracts – has mirrored sports volume ever since. Kalshi has been building upward in complexity, not branching sideways.

This matters for how Kalshi’s own figures read. In a June 19 interview with Front Office Sports, CEO Tarek Mansour said sports’ share of volume had been declining. He was citing a Dune query that tracks the Sports category alone and that for the week of June 8 had put sports at 53 percent. Our query, combining Sports and Exotics, puts that same week at 85.2 percent. The divergence is almost entirely Exotics. Mansour’s framing – that Kalshi is diversifying beyond sports – is less about the platform’s trajectory than about a product category’s label.

Revenue tells its own story

According to Yahoo Finance, which applied Kalshi’s published fee formula to its trading data via public API, 89 percent of Kalshi’s fee revenue across 2025 derived from sports: $234.6 million out of a total $263.5 million. That share rose as the year progressed; for the last four months it exceeded 90 percent. December alone generated $63.5 million.

Kalshi, being private, does not report its revenues. Its fee formula – general fee = 0.07 × C × P × (1–P), rounded up to the nearest cent, where C is the number of contracts and P is the contract price in dollars – peaks at an implied probability of 50 percent.

By May 2026 Dune data put Kalshi’s monthly fee revenue at $137.86 million, against $28.07 million for its nearest competitor, Polymarket. The research firm Sacra, which covers private companies, estimates Kalshi’s annualized revenue at approximately $2 billion as of June 2026 – up from $735 million in December 2025 and $25 million a year before that. In May Kalshi told Bloomberg its annualized revenue had exceeded $1.5 billion. The result has been money other than fees.

New funding

In May 2026 Kalshi raised $1 billion in a Series F round at a valuation of $22 billion. It was led by Coatue, with Sequoia Capital, Andreessen Horowitz, IVP, Paradigm, Morgan Stanley and Ark Invest taking part. The company said it would use the capital to expand into hedge funds, asset managers, proprietary trading firms and insurance companies. The round was the fifth since 2021.

Kalshi funding rounds, February 2021 to May 2026

| Date | Round | Amount |

|---|---|---|

| Feb 2021 | Series A | $30 million |

| Jun 2025 | Series C | $185 million |

| Oct 2025 | Series D | $300 million |

| Dec 2025 | Series E | $1 billion |

| May 2026 | Series F | $1 billion |

No Series B confirmed in any primary source.

What is Kalshi?

What Kalshi is not is a sportsbook. It takes no position on outcomes, sets no limits on winners, profits from no losses. Kalshi operates an exchange, matching buyers and sellers of binary event contracts: yes-or-no positions priced between one cent and 99 cents, paying out $1 if correct. Its revenue is a transaction fee from both sides regardless of result.

Because it issues futures contracts rather than accepting wagers Kalshi falls under the jurisdiction of a single federal agency, the Commodity Futures Trading Commission (CFTC), rather than under the patchwork of state gambling regulators – or so the argument has gone. The principle is being proved in the courts of nine states. (See our forthcoming article on “The legal war.”)

A word from the CEO

Mansour’s perspective on the opposition is direct. Traditional sportsbooks earn a margin of 15 to 20 percent by taking the other side of every bet; Kalshi earns roughly one percent in exchange fees. “If your competition is criticising you,” he told Front Office Sports in June, “that may be a good signal.”

On the role of Donald Trump Jr., a Kalshi adviser and Polymarket investor, Mansour was equally plain: no regulatory role, present for access and networks, the same function former secretaries perform at CME Group, Nasdaq and Cboe. “Kalshi, honestly, we’re kind of like single-issue people. If you’re pro-prediction markets, we love you.”

League business

The leagues have been taking notice, and taking positions. Giannis Antetokounmpo of the Milwaukee Bucks and Kyle Kuzma are investors in Kalshi; Saquon Barkley of the Philadelphia Eagles holds a stake in Polymarket, according to The Profile. Mansour says Kalshi is in talks with all major leagues, for two reasons: integrity (a data link, a ban on athletes trading in their own leagues) and fan engagement (80% of its users, he said, never trade at all). Whether the holdouts – the NFL chief among them – will ultimately sign is an open question. (See our forthcoming article on “The deals.”)

New challengers

The measure of what Kalshi has become arrived from an unexpected direction. On June 18 the Chicago Mercantile Exchange (CME Group), the largest derivatives exchange in the world, filed suit against the CFTC in the US District Court for the District of Columbia (Case 1:26-cv-02157). It is lodging a complaint against Kalshi’s recently approved bitcoin perpetual futures contract, arguing that it amounts to a swap, under the Dodd-Frank Act, rather than a futures contract and that the CFTC bypassed the required period for public comment to approve it. CME CEO Terrence Duffy spent eight months preparing the challenge. Kalshi is not a named defendant.

CME simultaneously distributes a competing prediction market product, FanDuel Predicts, launched with FanDuel in November 2025. The lawsuit is not a contradiction; it is a measure of how seriously the incumbents are taking an upstart firm from New York that colored a Presidential election and has swollen in five years into something the world’s largest exchange feels compelled to sue.

How we counted

Kalshi’s trading data is publicly accessible via its API, aggregated by Dune Analytics (dune.com) under the dataset kalshi.market_report. We queried weekly volume by category from platform launch through June 15, 2026 – combining the Sports and Exotics categories. To confirm Exotics’ composition, we examined all 100 available rows of Exotics data by contract type; all 100 were sports-derived (multi-game parlays, cross-category sports combiners, college basketball championship markets). Query saved at dune.com/queries/7798174.