The pet market is growing rapidly and, at around $270 billion, has long since reached the scale of the global sporting goods market. While large parts of the industry are dominated by pet food and veterinary services, the accessories and equipment segment in particular is opening up new opportunities for sports and outdoor companies. With Thule and Adidas, the first players have already begun to secure their share of the market.

No wonder, since the pet market is no longer a niche topic: By 2034, its volume could rise to around $500 billion. Estimates from various market researchers, such as Fortune Business Insights and Future Market Insights, consistently point to annual growth of around seven percent. More and more people are keeping pets and treating them like family members – and this is precisely where new segments are emerging. And the best part: the pet market presents itself as a strategically open playing field.

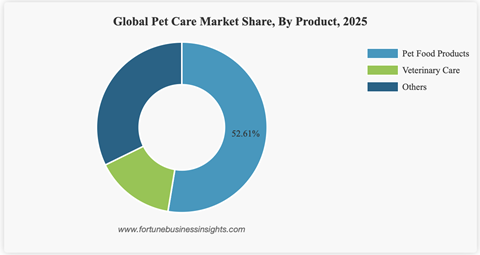

A $160-billion market – the relevant market segment

Even though pet food and veterinary services account for the majority, around one-third falls under the umbrella category “Others.” In this category, Fortune Business Insights includes, among other things, accessories, equipment, and thus also performance-oriented products. This already corresponds to a market value of around $90 billion today. If we apply the expected growth to this segment, the potential volume by 2034 will exceed $160 billion – an increase of around $70 billion.

Growth on par, a market with gaps

Compared to the global sporting goods market, this reveals another interesting dynamic: Not only is the pet market growing at least as fast, but the structural differences present opportunities. While the sporting goods market has been clearly segmented for years and dominated by established players, the part of the pet market relevant to sports and outdoor brands remains fragmented and largely opaque.

Dogs as the key to the market

This is precisely what drives the market’s dynamics. Rather than through clearly defined categories and metrics, the segment is currently evolving primarily through strategic positioning. For brands, it is less about defending existing market share and more about finding a role in the first place within a market that is not yet fully defined. Or about tapping into new business areas. Important to know: Dogs account for the largest market share at around 40 percent – and thus represent precisely the animal group that can be most easily integrated into sports and outdoor contexts.

Performance first: the role of specialized providers

But how exactly are brands tapping into this market? One initial approach comes from specialized providers for whom the pet market is their core business. A particularly exciting brand here is Non-stop dogwear, which clearly positions itself in the performance and outdoor segment. The Norwegian company launched in 2009 and has consistently tailored its offerings to active dog owners. Its focus includes harnesses for sports such as canicross, ski- and bikejoring, or trail running with dogs, often developed in close collaboration with athletes and a dedicated community.

Financially, the company remains within the typical range for specialized providers: According to Norwegian business registry data, revenue in 2024 was approximately NOK 215 million (about €19.5m), with a positive operating result. With 41 employees, the organization remains lean, underscoring the segment’s early stage of development. Nevertheless, Non-stop dogwear is one of the fastest-growing companies in Europe: In the 2025 FT 1000 of Europe’s fastest-growing companies, the firm ranked 13th in the retail sector. According to the Financial Times, this is based on the average annual revenue growth rate between 2020 and 2023.

Even established specialists like Ruffwear (founded in 1994 in Oregon, USA) achieve a comparatively modest scale with annual revenue of around $23 million. Other providers are also estimated to be in the double-digit million range, without disclosing their figures in detail. In relation to a market volume of around $90 billion, it becomes clear that the business is spread across a large number of small and medium-sized providers – clear market leaders are hardly discernible so far.

Europe as the hub of performance brands

Similar approaches are pursued by providers such as Hurtta (Finland), Zero DC and Manmat (both Czech Republic), or Back on Track (Sweden), each of which has grown out of specific application areas and places a strong emphasis on functionality and community. Unlike large consumer goods companies, the product here does not emerge from a category but from specific usage scenarios in everyday life and sports. This is precisely how these brands build credibility and loyalty. In their role, they are reminiscent of early specialists in the running market such as On, Hoka, or Salomon in trail running, which initially occupied clearly defined niches and scaled up from there.

In general, it is also noticeable that the dog gear segment has a strong European influence: many specialized providers come from Scandinavia or Central Europe, where outdoor activities with four-legged companions traditionally play a major role. In the U.S., on the other hand, brands like Ruffwear or Kurgo take a more lifestyle- and mobility-oriented approach, focusing on everyday life with dogs.

Traveling with dogs: a champion candidate at Thule

A second model is emerging among companies that view the pet sector as a functional extension of their existing business. The publicly traded Swedish company Thule is a prime example of this: Building on its core expertise in transport and mobility solutions, the company is expanding its portfolio to include products for the safe and comfortable transport of dogs. This makes the canine companion part of existing usage scenarios – such as traveling, cycling, or everyday life in the car. In its 2025 annual report, Thule emphasizes that dog transportation is one of the “champion candidates” – that is, a category expected to be among the most important growth drivers in the future. The Swedish manufacturer aims to significantly expand this category by 2035. CEO Mattias Ankarberg explains: “Products for dog transport, which had a record-breaking start in 2024, have continued to perform strongly, helped by the launch of more products.”

From product to lifestyle

In this case, “Pet” is not a standalone business segment, but a logical extension based on existing customer needs. Growth thus stems less from new target groups than from the expansion of existing usage chains. This logic is also reflected in the segment structure: While Thule initially grouped the entry under “Juvenile & Pet Products,” the category was later renamed “Active with Kids & Dogs” – a step toward usage contexts and lifestyles rather than traditional product categories.

Within the “Active with Kids & Dogs” segment, which accounts for approximately 100 million euros in revenue according to the 2025 annual report, the share of the dog business is currently estimated to be between 20 and 40 million euros. This means that, despite the size of its corporate group, Thule operates at a similar level to specialized providers in the pet sector. This underscores the fact that even billion-dollar corporations have so far only tapped into the pet market in select areas.

Adidas: lifestyle over performance

Which brings us to industry giants like Adidas. Quietly and largely in the background, they too are entering the pet market. But initially, this serves more as a testing ground for brand loyalty and new target groups – far removed from their core business. Collections for dogs and cats are not primarily viewed as functional gear, but rather as part of an overarching lifestyle concept – often in the spirit of a “Mini-Me” approach between humans and animals. The German company uses this as an extension of its brand universe, relying heavily on emotional appeal and cultural trends.

As early as 2025, Adidas ramped up these efforts with targeted launches. In October, the brand unveiled its Fall/Winter 2025 Pet Collection – garments that, for the first time, went well beyond a purely apparel-focused approach. In addition to classic track tops, the collection also included more functional products such as vests, windbreakers, and even accessories like backpacks. The central idea remained clearly recognizable: the application of iconic Adidas design codes to pets and the portrayal of shared experiences between humans and animals in the spirit of the “Mini-Me” concept.

Adidas took it a step further at the end of the year: With the “China Tracktop Pet Collection,” launched exclusively in China in late December 2025, the company specifically linked its pet strategy to regional cultural and lifestyle trends. The collection drew on design elements from traditional Chinese clothing and translated them into the familiar Adidas Originals aesthetic – once again with the goal of creating visual unity and an emotional connection between humans and animals.

The biggest market lies in the food bowl – take Doppelherz, for example

A fourth, hitherto less-noticed approach comes from the health and dietary supplement sector. According to estimates, this corresponds to a segment of approximately $140 to $160 billion – based on a total volume of around $270 billion (in 2025). And thus, it is the industry’s growth driver.

Doppelherz demonstrates that this approach works: The global brand entered the pet market as recently as 2021 with its own pet line, thereby tapping into a new business segment in a short period of time. The German company has thus successfully transferred its expertise from the human sector to pets and opened up another growth area. Even though the segment is still small within the corporate context, it is strategically relevant: Queisser Pharma, the company behind Doppelherz, generates around 380 million euros in revenue but does not report the pet segment separately – an indication that it is still a young but growing business area. The focus here is not on activity or equipment, but on health, prevention, and well-being.

Supplements for animals: a market for new entrants

This is precisely what creates an interesting parallel to the sports industry in this segment: the substantive similarity between dietary supplements for humans and for animals is significantly greater than between traditional sports equipment and pet products. When companies like Doppelherz enter the pet market, the question inevitably arises: why shouldn’t manufacturers from the sports nutrition segment follow suit? Especially since the market is currently (still) very open: even providers from outside the industry can enter relatively easily and occupy new sub-segments.

Outdoor reimagined: The dog as part of the system

A fifth, as yet largely untapped avenue lies within the traditional outdoor segment itself. For brands like The North Face, Patagonia, or Deuter, this is less about a new target audience and more about expanding existing usage systems. Those traveling with dogs have different equipment requirements: tents must be designed to be more robust and spacious, sleeping systems must offer protection and comfort for both humans and animals, and backpacks must integrate additional features. The dog thus becomes part of the setup – and opens up an obvious, yet so far scarcely systematically developed, business segment. Precisely because many solutions are still improvised today, this represents one of the most direct growth opportunities for the outdoor industry.

Sports, mobility, pets: lifestyles converge

The pet market thus seems tailor-made for emotional products – and for brands that occupy entire lifestyles. After all, consumers are increasingly thinking in such contexts rather than in terms of individual product categories. Activities like running, hiking, or traveling are increasingly being planned together with the dog – and accordingly, new product offerings are emerging that combine sports, mobility, and pet supplies.

From product to use: how competition is shifting

This shift is already evident in the sports industry: For example, Decathlon is strategically focusing on linking sports and technology through partnerships such as its collaboration with MediaMarktSaturn – currently limited to Germany – and is aligning its offerings more closely with holistic usage contexts rather than traditional product categories. Thule is also following this logic by consistently structuring its categories around usage scenarios rather than product groups. As a result, competition in the pet segment will increasingly be decided not by individual products, but by the ability to play a credible role in the daily lives of active pet owners.

Topics

- Adidas

- Adidas Originals

- Back on Track

- Decathlon

- Deuter

- Doppelherz

- Fortune Business Insights

- Future Market Insights

- Hoka

- Hurtta

- Kurgo

- Mammat

- Market Analysis

- MARKET DEVELOPMENT

- Market Statistics

- Mattias Ankarberg

- MediaMarktSaturn

- Non-stop dogwear

- On

- Patagonia

- Product

- Queisser Pharma

- Ruffwear

- Salomon

- The North Face

- Thule

- Zero DC